》Check SMM aluminum product quotes, data, and market analysis

》Subscribe to view historical spot prices of SMM metals

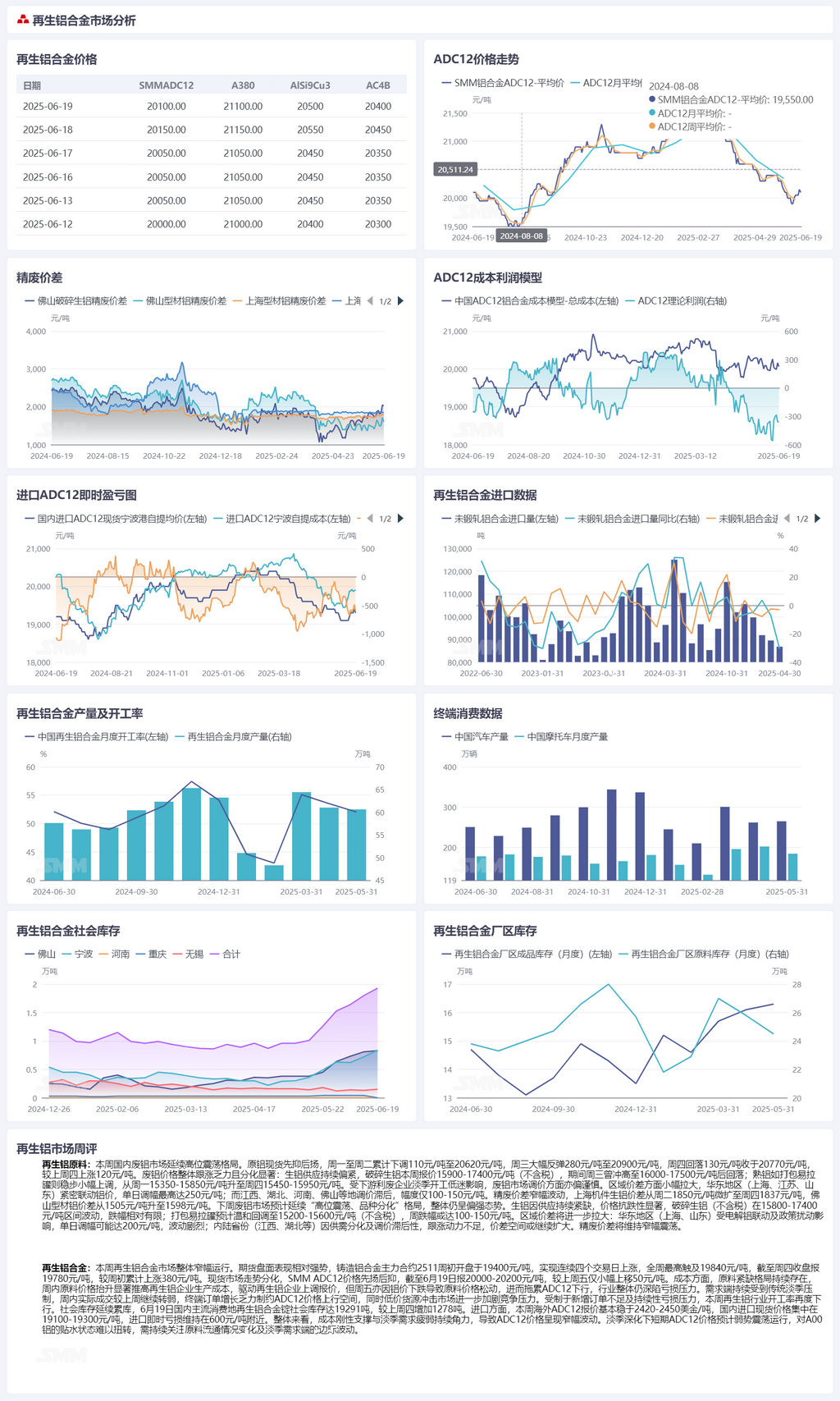

Secondary aluminum raw materials:

This week, the domestic aluminum scrap market continued to fluctuate at highs. Spot primary aluminum first declined and then rose, cumulatively falling by 110 yuan/mt to 20,620 yuan/mt from Monday to Tuesday, before rebounding sharply by 280 yuan/mt to 20,900 yuan/mt on Wednesday. It then pulled back by 130 yuan/mt to close at 20,770 yuan/mt on Thursday, up 120 yuan/mt from last Thursday. Aluminum scrap prices generally struggled to catch up and showed significant divergence: aluminum tense scrap supply remained tight, with quotes for shredded aluminum tense scrap ranging from 15,900-17,400 yuan/mt (tax excluded) this week, peaking at 16,000-17,500 yuan/mt on Wednesday before pulling back. Wrought aluminum alloy scrap, such as baled UBC, steadily increased slightly, rising from 15,350-15,850 yuan/mt on Monday to 15,450-15,950 yuan/mt on Thursday. Affected by the low operating rates of downstream scrap utilization enterprises during the off-season, the aluminum scrap market was also cautious in adjusting prices. Regional price spreads widened slightly, with east China (Shanghai, Jiangsu, Shandong) closely following aluminum price movements, with daily adjustments of up to 250 yuan/mt. In contrast, regions like Jiangxi, Hubei, Henan, and Foshan lagged in price adjustments, with ranges of only 100-150 yuan/mt. The price difference between A00 aluminum and aluminum scrap fluctuated rangebound, with the price spread for mechanical casting aluminum scrap in Shanghai slightly expanding from 1,850 yuan/mt on Tuesday to 1,837 yuan/mt on Thursday, and the price spread for mixed aluminum extrusion scrap free of paint in Foshan rising from 1,505 yuan/mt to 1,598 yuan/mt. Next week, the aluminum scrap market is expected to continue the pattern of "fluctuating at highs with divergence among varieties," remaining generally strong. Due to persistent supply tightness, aluminum tense scrap prices will show significant resilience, with shredded aluminum tense scrap (tax excluded) fluctuating within the range of 15,800-17,400 yuan/mt, with relatively limited declines. Baled UBC is expected to experience a mild pullback to 15,200-15,600 yuan/mt (tax excluded), with a possible weekly decline of 100-150 yuan/mt. Regional price spreads will further widen: east China (Shanghai, Shandong) may see daily adjustments of up to 200 yuan/mt due to the linkage with primary aluminum and policy disturbances, resulting in significant fluctuations. Inland provinces (Jiangxi, Hubei, etc.) may lack the momentum to catch up due to supply and demand divergence and lagging price adjustments, potentially leading to a continued expansion of price spreads. The price difference between A00 aluminum and aluminum scrap will continue to fluctuate rangebound.

Secondary aluminum alloy:

This week, the secondary aluminum alloy market generally operated within a narrow range. The futures market performed relatively strongly, with the most-traded cast aluminum alloy 2511 contract opening at 19,400 yuan/mt at the beginning of the week and rising for four consecutive trading days, reaching a high of 19,840 yuan/mt during the week. It closed at 19,780 yuan/mt on Thursday, up a cumulative 380 yuan/mt from the beginning of the week. The spot market showed divergence, with SMM ADC12 prices first rising and then falling, closing at 20,000-20,200 yuan/mt on June 19, up only slightly by 50 yuan/mt from last Friday. On the cost side, the shortage of raw materials persisted, and the significant increase in raw material prices during the week pushed up the production costs of secondary aluminum enterprises, driving them to raise their quotes. However, on Friday, the decline in aluminum prices led to a loosening of raw material prices, which in turn dragged down ADC12 prices. The industry as a whole remained under significant pressure from losses. Demand side, it continued to be suppressed by the traditional off-season, with actual transactions during the week continuing to weaken compared to the previous week. The lack of growth in end-user orders constrained the upside room for ADC12 prices, while the influx of low-priced supplies further intensified competitive pressure. Due to insufficient new orders and sustained pressure from losses, the operating rate of the secondary aluminum industry declined again this week. Social inventory continued to build up, with the social inventory of secondary aluminum alloy ingots in domestic mainstream consumption areas reaching 19,291 mt on June 19, an increase of 1,278 mt from Thursday of the previous week. In terms of imports, overseas ADC12 quotes remained largely stable at USD 2,420-2,450/mt this week, while domestic import spot prices were concentrated in the range of 19,100-19,300 yuan/mt, with immediate import losses hovering around 600 yuan/mt. Overall, the rigid support from costs and the weak demand during the off-season continued to clash, leading to a fluctuation rangebound in ADC12 prices. With the off-season deepening, ADC12 prices are expected to remain in the doldrums in the short term, and the discount to A00 aluminum is unlikely to reverse. Continuous attention should be paid to changes in the circulation of raw materials and marginal fluctuations in demand during the off-season.